- CQF Program

- Events

- Resources »

- Membership

- Careers »

- About Us »

Open Filter

Boris Johnson, Yanis Varoufakis And Sir Vince Cable All Have Something In Common

In Dr. Paul Wilmott's latest blog post he highlights what Boris Johnson, Yanis Varoufakis and Sir Vince Cable all have in common as they give their views on Brexit.

Mon 25 Sep 2017

IMPACT STUDY: Earnings Sentiment Consistently Outperforms Consensus

In RavenPack’s latest research, we find that their new earnings sentiment indicator derived from real-time news and social media significantly outperforms consensus estimates.

Tue 12 Sep 2017

How to use Natural Language Processing for Multi-Topic Quant Investing

In this article, Peter Hafez discusses how investors need the right tools to cut through the noise to uncover the signal behind the latest move in the markets.

Wed 23 Aug 2017

Navigating Stock Market Crashes in the Brexit Trump Era (Presentation Slides)

Presentation slides for Dr. Bill Ziemba's talk - 'Navigating Stock Market Crashes in the Brexit Trump Era'.

Wed 31 May 2017

Shiny New Toys: Does Wealth Management Need A.I.?

In this article, Greg Davies examines the allure of adopting artificial intelligence as a solution for a range of business problems in Wealth Management and the need to appropriately match solutions to problems.

Tue 30 May 2017

Stock Market Crashes in 2007 - 2009: Were We Able to Predict Them?

In this article, Sebastien Lleo and William T. Ziemba investigate the stock market crashes in China, Iceland and the US in the 2007 - 2009 period.

Mon 27 Mar 2017

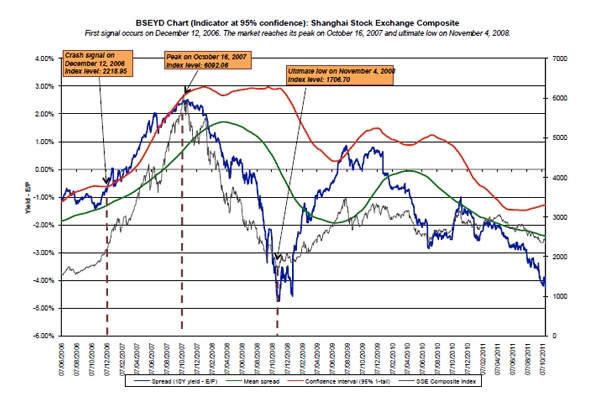

A Tale of Two Indexes Predicting Equity Market Downturns in China

Sebastien Lleo and William T. Ziemba investigate whether traditional crash predictors, predicts crashes for the Shanghai Stock Exchange Composite Index and the Shenzhen Stock Exchange Composite Index.

Mon 20 Mar 2017

Sell in May and Go Away in the Equity Index Futures Markets

Constantine Dzhabarov and William T. Ziemba explain when the best time is to sell in the index futures markets.

Mon 13 Mar 2017

Index-tracking Portfolio Optimization Model

In the present tutorial report Guillermo Navas-Palencia examines the theory and computational aspects behind the index-tracking portfolio optimization model.

Thu 24 Nov 2016

Intellectual Property Law: A Briefing for Quants

In this article Barbara Mack gives a briefing for Quants on the Intellectual Property Law, covering the U.S. intellectual property regime, and the four types of protectable assets: copyright, trademark, trade secret and patent.

Fri 23 Sep 2016